Major U.S. banks slashed their savings rates immediately after the Federal Reserve’s ($FED) October 2025 rate cut, sending rates toward their lowest levels since early 2022. The focus keyphrase—savings rates after Fed cut—now commands renewed attention as yields sink faster than analysts predicted. What risks do savers and investors now face?

U.S. Bank Savings Rates Tumble to 1.4% After Fed’s 0.25% Cut

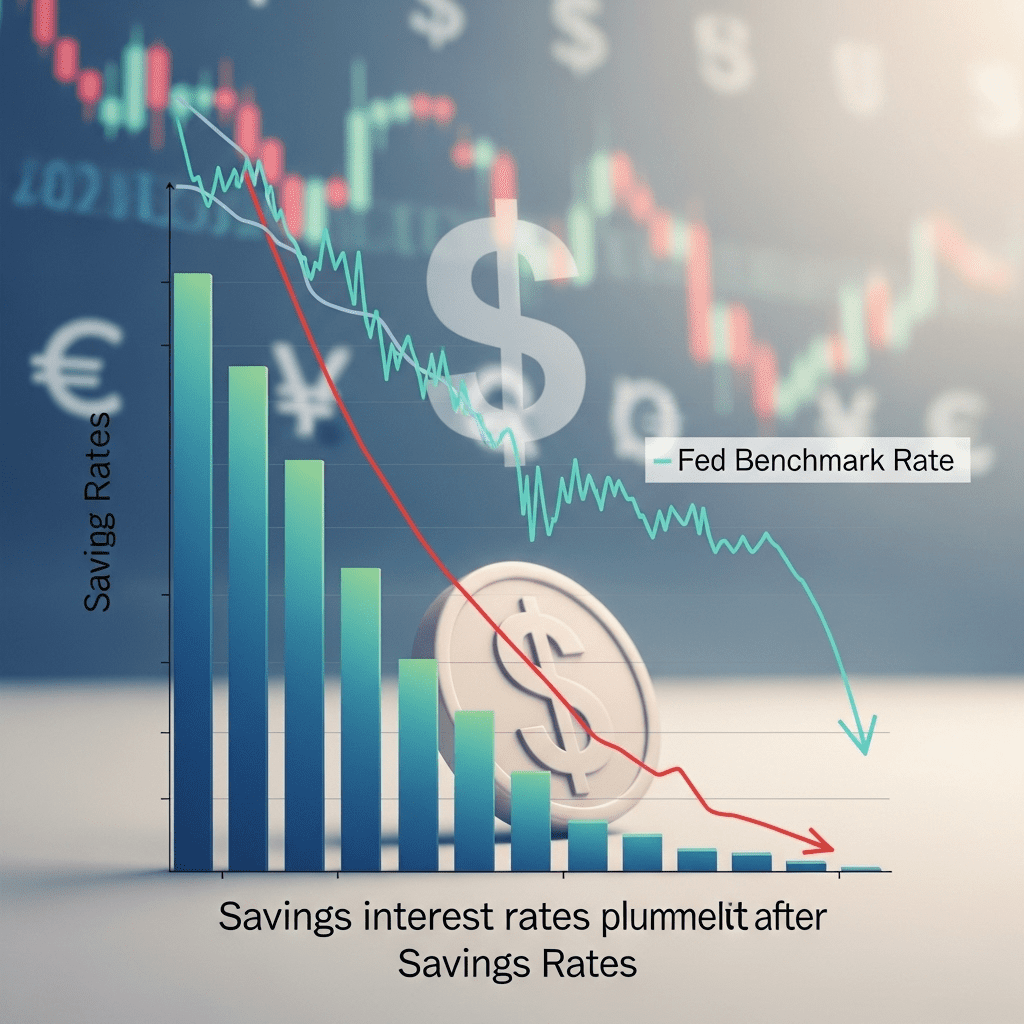

The Federal Reserve ($FED) announced a 0.25% benchmark rate cut on October 29, 2025, pushing its target federal funds range to 4.75%-5.00%—the first move since the last hike in July. In response, leading commercial banks including JPMorgan Chase & Co. ($JPM) and Bank of America Corp. ($BAC) reduced their national average savings account rates to 1.4%, down from 1.65% a week earlier, according to FDIC data released on October 29. This acceleration marks the steepest weekly decline since mid-2023 (FDIC Weekly National Rates Report, Oct. 2025). Online banks, which had been offering over 4% APY on savings as recently as August, are now quoting rates between 2.10%-2.50% as of October 30 (Bankrate, Oct. 2025).

Why Lower Savings Rates Could Pressure Household Wealth in 2025

The drop in savings rates intensifies pressure on household wealth, especially as inflation remains above the Fed’s 2% target. Real returns on savings accounts have turned increasingly negative, with July-September 2025 CPI data showing annual inflation at 2.6% (U.S. Bureau of Labor Statistics). In historical context, average U.S. savings account yields dipped below 1% during the 2020-2021 pandemic easing cycle, a trajectory some economists see repeating if further cuts follow. A report from Moody’s Analytics in September 2025 indicated that about $6.2 trillion in U.S. household deposits are now eroding in real value, raising long-term concerns for consumer purchasing power and retirement savings.

How Investors Can Adjust Portfolios as Savings Rates Decline

With savings rates after the Fed cut sliding, investors seeking yield must pivot. Many are reallocating cash from traditional deposit accounts into short-term Treasury securities, where yields stood at 4.2% for 3-month T-bills as of October 29 (U.S. Treasury data). Money market funds also remain attractive, averaging 4.05% returns (Investment Company Institute, Oct. 2025). However, as rates decline, risk appetite may rise: equity income funds and dividend stocks such as Procter & Gamble ($PG) and Johnson & Johnson ($JNJ) could see renewed interest despite heightened market volatility. For continuous analysis on shifts in investor positioning, see our latest financial news or browse our investment strategy section. Savers should remain vigilant for promotional offers from online banks, though these deals may prove fleeting in a declining-rate environment.

What Analysts Expect for Savings Yields After the Fed’s Shift

According to analysts at Wells Fargo and data from Morningstar, U.S. savings rates could fall below 1% by early 2026 if the Fed pursues another cut by year-end—a scenario deemed likely by CME FedWatch Tool probabilities (as of October 28, 2025, anticipating a 57% chance of another 0.25% cut within the next two meetings). Industry analysts observe that banks, facing shrinking net interest margins, historically reduce savings yields aggressively during easing cycles to protect profitability. This pattern suggests rates may undershoot current forecasts if policy signals remain dovish.

Why the Fed’s Rate Cut Signals a New Era for Savings Rates

The Fed’s latest move has fundamentally reset expectations for savings rates after Fed cut, introducing new risks for conservative investors and savers. Monitoring future policy guidance, inflation reports, and bank earnings will prove critical as the savings landscape evolves. For now, investors should prepare for a prolonged low-yield environment—making portfolio diversification and rate-shopping top priorities.

Tags: savings rates, federal reserve, bank stocks, interest rate cut, investor strategy