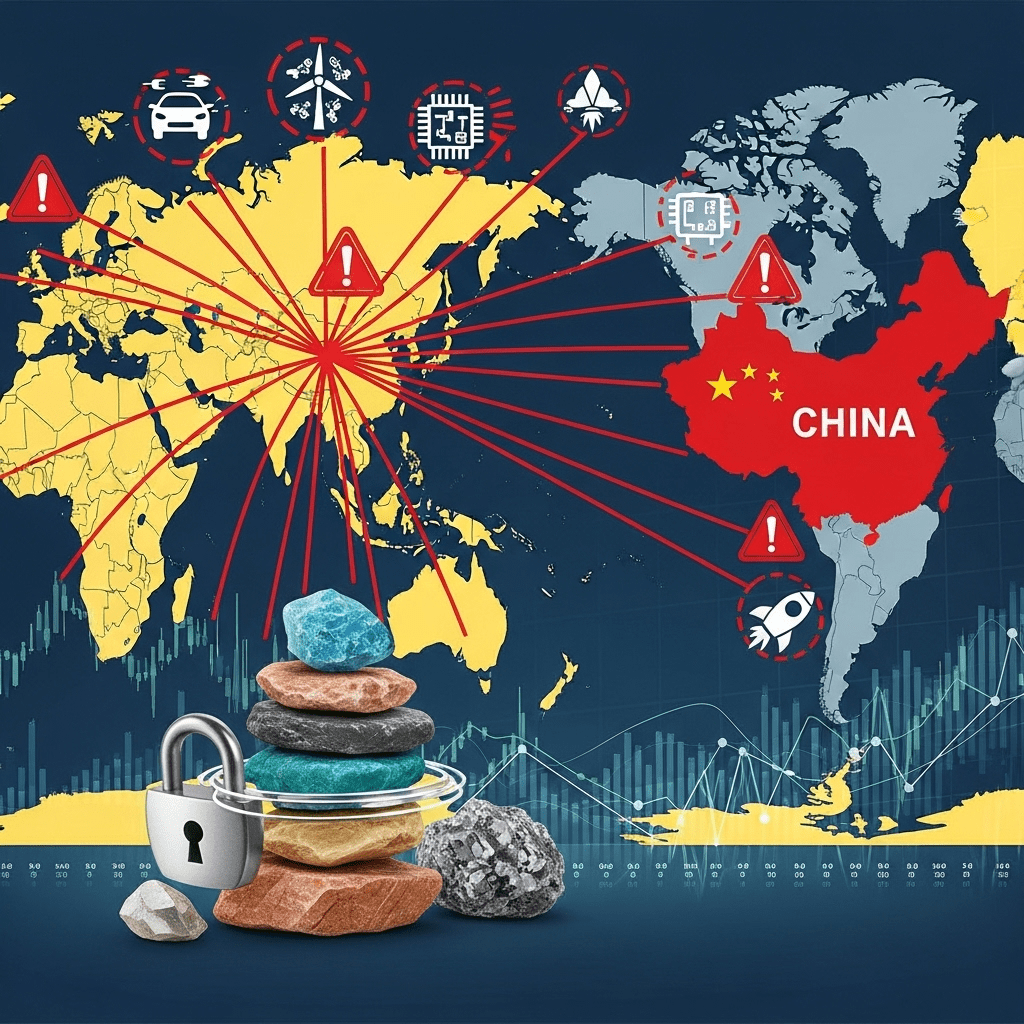

In a bold move, China unveiled sweeping policies to control rare-earth exports. The decision aims to protect national security and preserve China’s dominance in strategic minerals. As the world’s top supplier, China’s actions ripple across industries—from electronics to renewable energy and defense. In 2025, these changes are expected to reshape global supply chains.

Key Facts: China’s Rare-Earth Export Controls and Motivations

China’s Ministry of Commerce announced strict export rules for rare-earth elements, citing national security concerns. Rare earths are essential for electric vehicles, advanced electronics, defense systems, and renewable energy.

The new controls require exporters to undergo detailed screening and obtain licenses. Companies must report supply chain data, verify end-use with foreign buyers, and meet environmental and technology standards. These measures reinforce China’s oversight of strategic resources and strengthen its leverage in global trade.

Implications for Global Markets and Industries

The announcement caused immediate volatility in rare-earth prices. Manufacturers in automotive, aerospace, defense, and clean energy sectors are particularly affected. China controls more than 80% of processed rare earths, so any policy shift carries significant weight.

Countries are responding by diversifying supply chains. Domestic mining, recycling, and alternative sourcing are gaining priority. For investors, these developments present both risks and opportunities. Monitoring policy shifts is now critical for companies and funds. For more

investment insights, staying informed is essential.

Geopolitical Drivers Behind China’s Policy

Experts link China’s controls to rising trade tensions with the US, EU, and other partners. Rare earths are a strategic “chokepoint” resource. Export restrictions reinforce national security, safeguard proprietary technologies, and signal China’s willingness to use economic tools diplomatically.

For global investors, understanding these geopolitical dynamics is key. Regulatory uncertainty and export bans can affect pricing, valuations, and project feasibility. Tracking

macro trends helps develop resilient strategies.

International Responses

The US, Japan, and EU have pledged to strengthen supply chain resilience. Initiatives include boosting domestic production, forging new partnerships, and investing in rare-earth alternatives.

Analysts predict that mining outside China—in Australia, Canada, and Africa—will expand. Scaling production is a multi-year challenge, due to environmental, technical, and financial barriers. Transparency, ESG compliance, and long-term contracts are now critical for buyers and suppliers. For deeper guidance, see

global market strategies.

Future Outlook: Navigating Rare-Earth Market Uncertainty

China’s new export controls introduce uncertainty. Short-term price spikes and supply shortages are likely, especially for industries with limited alternatives.

Over time, enhanced coordination, innovation in extraction and recycling, and research investments may create a more resilient ecosystem. Manufacturers and investors must monitor developments closely. The ability to adapt to geopolitical shocks will be key to maintaining competitiveness in critical mineral markets.