Major lenders including JPMorgan Chase ($JPM) revealed HELOC rates today, November 15, 2025, have risen to the highest levels since early 2008, reaching an average of 8.05%. With millions still holding low-rate primary mortgages, the spike in HELOC rates today brings both opportunity and risk for U.S. homeowners. Why are more Americans drawing cash now?

HELOC Rates Jump to 8.05% in November—Highest Since 2008

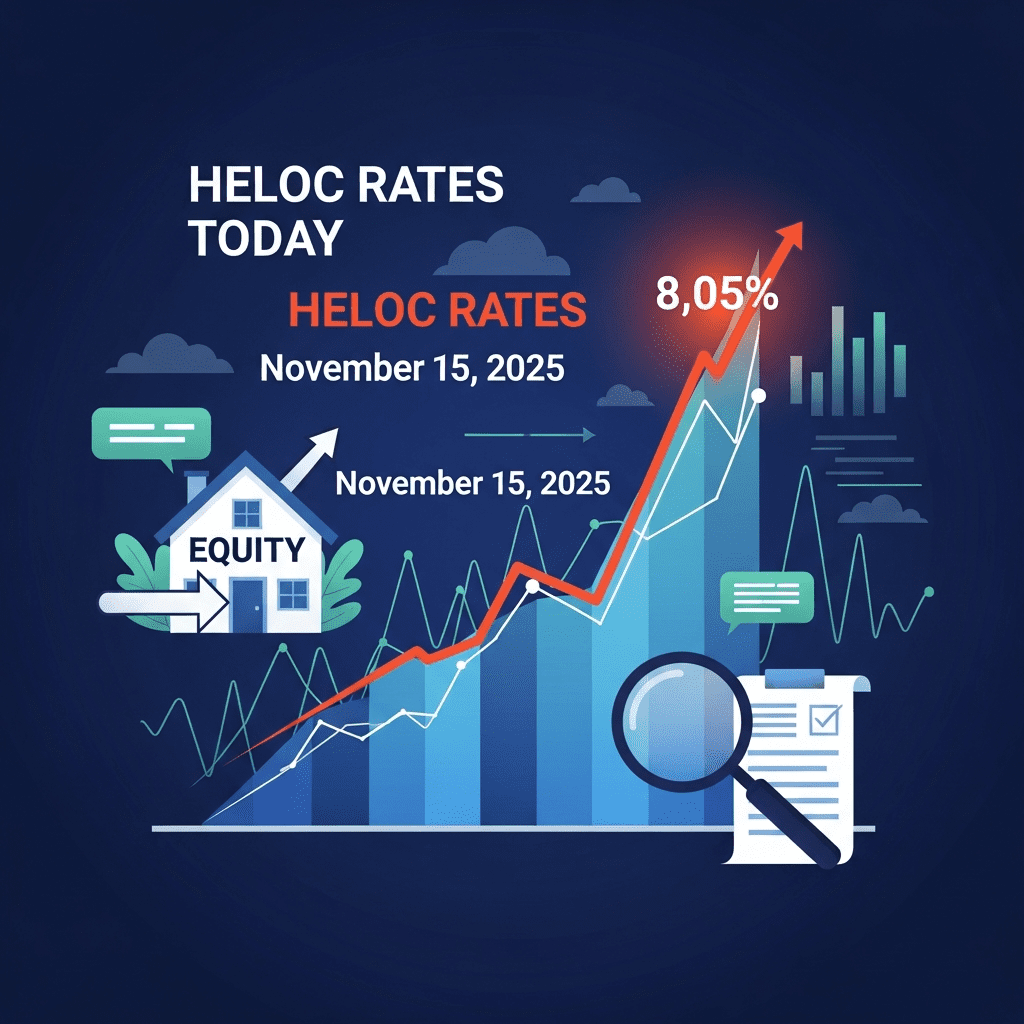

Home equity line of credit (HELOC) rates averaged 8.05% across major U.S. lenders on November 15, 2025—up 23 basis points from one month prior, according to Bankrate and Freddie Mac weekly mortgage surveys. For context, HELOC rates stood at 7.02% on January 1, 2025, and have surged over 100 basis points since last spring. JPMorgan Chase ($JPM) and Bank of America ($BAC) both confirmed prime-based HELOC rates now exceed 8% for the first time since the global financial crisis, following the Federal Reserve’s persistent stance on higher-for-longer policy rates (Bloomberg, Nov. 2025). Lenders report increased application volumes as property owners avoid refinancing historically low primary mortgages, typically locked in under 4% between 2020 and early 2022.

Why Higher HELOC Rates Reshape U.S. Housing and Lending Markets

The sharp rise in HELOC rates today draws new dividing lines in the housing finance sector. According to the Mortgage Bankers Association, more than 72% of current mortgage holders maintain rates below 4%, making HELOCs a preferred—but pricier—option for cash access. This dynamic has prompted U.S. home equity borrowing to climb 14.7% year-over-year through Q3 2025 (Equifax U.S. Consumer Credit Trends, October 2025). Meanwhile, higher HELOC costs may exert downward pressure on consumer spending, with household debt payments nearing decade highs per Federal Reserve data. Broader market volatility—driven by Fed monetary policy and persistent inflation—continues to impact the cost and demand for home equity credit lines.

How Investors and Homeowners Can Navigate Rising HELOC Rates

For investors and portfolio managers, the surge in HELOC rates today, November 15, 2025, demands renewed scrutiny of exposure to housing and consumer credit sectors. Lenders such as Wells Fargo ($WFC) and regional banks may benefit from wider lending margins but also face delinquency risk if borrowing costs rise faster than incomes. Homeowners looking to tap equity should carefully compare rate structures, upfront fees, and potential tax deductibility rules. Retaining a low-rate primary mortgage while accessing cash via HELOCs remains attractive, but variable rates add uncertainty. For more, see our stock market analysis and the latest financial news on lending sector trends. Equity investors may want to watch financial sector ETFs and credit risk signals as HELOC volumes shift.

Market Analysts See HELOC Rate Plateau as Fed Policy Shifts Loom

Industry analysts observe that HELOC rates could stabilize if the Federal Reserve signals a policy reversal by early 2026. Market consensus suggests the current 8.05% average HELOC rate may mark a near-term peak, as inflation readings show signs of moderation and the Fed pauses further hikes. An unexpected surge in consumer defaults or a sharp decline in housing prices could, however, disrupt these expectations, keeping financial sector risk elevated.

HELOC Rates Today Signal New Risks and Strategies for 2025 Investors

Surging HELOC rates today, November 15, 2025, underscore the shifting landscape for homeowners and market participants alike. As borrowing costs climb, investors should monitor Fed moves, consumer credit health, and housing market data. Expect HELOC rates today, November 15, 2025, to remain a bellwether for broader credit and sector volatility in the months ahead.

Tags: HELOC rates, $JPM, mortgage lending, interest rates, stock market